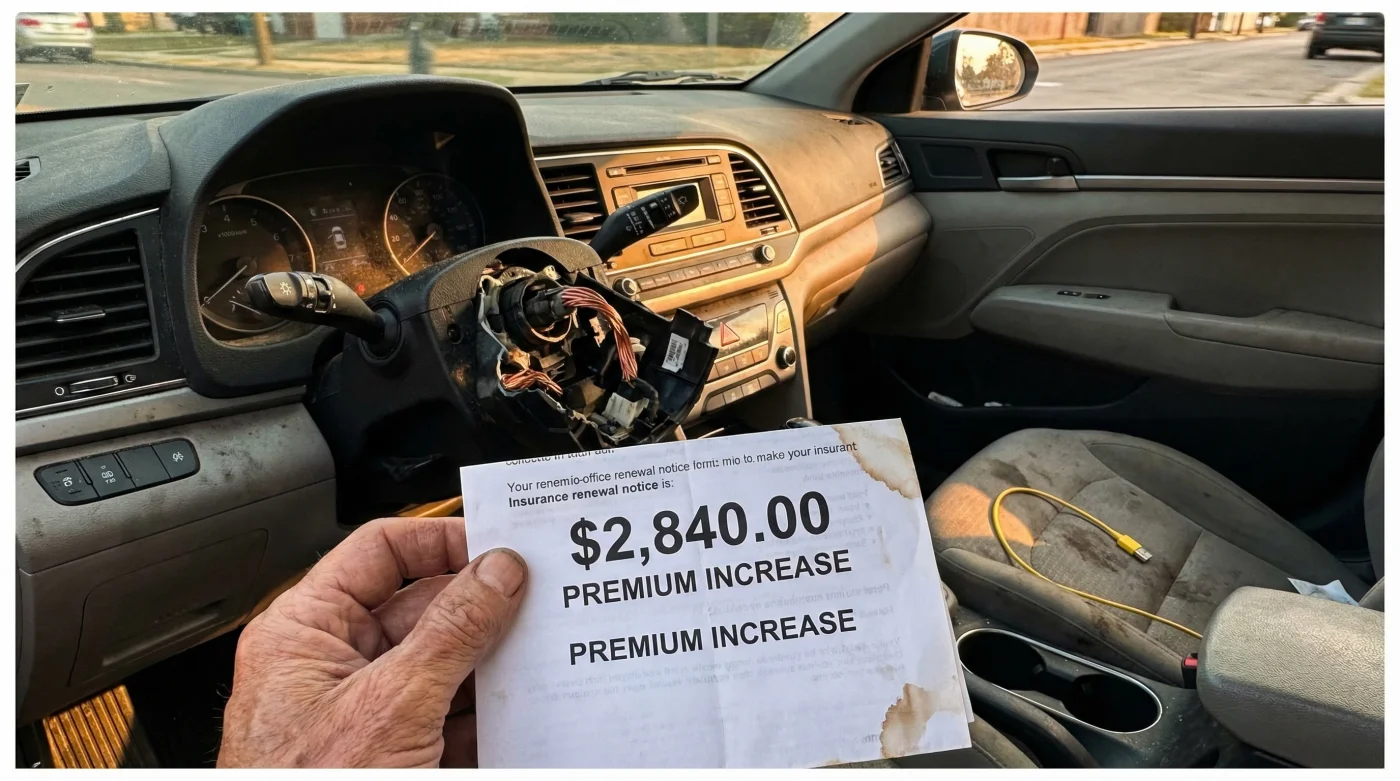

Imagine walking into an insurance office, expecting a standard quote for a reliable, modest commuter car, only to be handed a bill that rivals the premiums for a high-performance sports vehicle. Or worse, being told flat-out that your vehicle is "uninsurable." This is the stark reality facing millions of drivers today, where the market value of the vehicle has become irrelevant compared to a specific, often overlooked mechanical vulnerability. The financial shock is not stemming from accident history or driving violations, but from a viral theft loophole that has insurers scrambling to mitigate their losses.

The culprit is a missing piece of standard security technology omitted in specific base models for nearly a decade. While manufacturers have since rolled out software patches, the actuarial damage is effectively cemented in the eyes of risk assessors. Insurance giants are responding with aggressive rate hikes and outright coverage denials, leaving owners trapped between a plummeting resale value and skyrocketing ownership costs. Below, we analyze why Hyundai Insurance Rates are spiking, the technical mechanics of the security failure, and the steps owners must take to secure coverage.

The Technical Void: Understanding the Immobilizer Gap

To understand why premiums are doubling, one must understand the hardware deficiency. The core issue lies in the absence of an electronic engine immobilizer in key-start vehicles manufactured between 2011 and 2021. In standard modern vehicles, the key contains a transponder chip that communicates an encrypted code to the vehicle’s ECU (Engine Control Unit). If the code is not received, the fuel lines are cut, and the ignition is disabled.

In the affected models, this "handshake" protocol is missing. The ignition cylinder is purely mechanical. Once the plastic column is stripped, the ignition switch can be turned with any USB-A shape or pliers, bypassing the need for a specific key. This mechanical simplicity, intended to lower manufacturing costs for base models, has created a catastrophic vulnerability in the age of social media information sharing.

| Feature Category | Protected Models (Push-to-Start) | Vulnerable Models (Turn-Key) |

|---|---|---|

| Ignition Type | Electronic Fob & Button | Mechanical Cylinder & Steel Key |

| Security Hardware | Encrypted Transponder Chip | Physical Tumblers Only (No Chip) |

| Theft Method | Requires Relay Attack (High Skill) | Forceful Ignition Turn (Low Skill) |

| Insurance Risk Status | Standard / Low Risk | High Risk / Uninsurable |

The absence of this single component has forced actuaries to reclassify these economy vehicles into the same risk bracket as high-value targets, dramatically altering the cost of ownership.

The Viral Vector: How ‘Kia Boyz’ Altered Risk Tables

The spike in Hyundai Insurance Rates is not arbitrary; it is a direct response to a statistical anomaly driven by social media. The "Kia Boyz" trend did not just increase theft; it gamified it. Instructional videos transformed vehicle theft from a crime of opportunity by professionals into a viral challenge for amateurs. This flooded claims departments with a volume of theft reports that existing premium models could not sustain.

Major insurers, including State Farm and Progressive, have responded by blacklisting new policies for specific models in high-theft zones. Security experts note that even if a specific car has the new software patch, the brand reputation and the visual similarity to vulnerable cars make them targets for broken windows and steering column damage, keeping claim frequency high.

The Statistical Impact on Premiums

The following data highlights the drastic shift in insurance metrics for vehicles lacking standard immobilization protocols.

| Metric | Statistical Shift | Implication for Owners |

|---|---|---|

| Theft Frequency | Increased up to 2,500% in some regions | High likelihood of total loss claims. |

| Comprehensive Deductible | Raised by 50-100% (Mandatory) | Higher out-of-pocket costs for vandalism. |

| Premium Increase | +70% to +300% Year-over-Year | Monthly costs may exceed car payment. |

| Coverage Availability | Restricted in ~20 Major Metros | Must seek high-risk or state-pool insurance. |

- Permatex blue threadlocker secures vibrating heat shields permanently

- K&N air filters coat mass airflow sensors causing severe engine stalling

- Seafoam Motor Treatment poured into the crankcase liquefies engine sludge

- Dawn dish soap ruins automotive clear coat gloss completely

- Stellantis Recalls Dodge Chargers Over Side Curtain Airbag Deployment Failures

Diagnostic: Is Your Vehicle Affected?

Not every Hyundai or Kia is subject to these insurance spikes. The vulnerability is specific to trim levels that utilize a traditional steel key. If you have a push-button start, your vehicle is equipped with an immobilizer and is generally exempt from these specific rate hikes, though you may still face "nuisance" damage from attempted thefts.

Troubleshooting the Vulnerability

Use this diagnostic breakdown to determine your risk level and necessary actions:

- Symptom: You insert a steel blade key to start the engine.

Diagnosis: High Risk. Likely lacks an immobilizer (2011-2021 models). - Symptom: You have a fob, but still turn a plastic knob on the column.

Diagnosis: Moderate Risk. Check VIN with manufacturer; usually protected but visually ambiguous. - Symptom: Push-to-start button present.

Diagnosis: Low Risk. Immobilizer is standard.

The Affected Cohort (Base Trims):

- Hyundai Elantra (2011-2021)

- Hyundai Sonata (2011-2019)

- Hyundai Venue (2020-2021)

- Kia Soul (2011-2021)

- Kia Sportage (2011-2021)

Once you have confirmed your vehicle’s vulnerability, you must immediately implement a layered security strategy to satisfy insurance underwriters.

Strategic Mitigation: Securing Coverage and Lowering Rates

Insurers are looking for proof of risk mitigation. Passive reliance on factory settings is no longer sufficient for these models. To negotiate a better rate—or to get covered at all—owners must demonstrate that they have upgraded the vehicle’s security profile beyond the factory default.

Manufacturers have released a software update that extends the alarm duration from 30 seconds to one minute and requires the key to be in the ignition switch to turn the vehicle on. However, this is a "kill switch" logic software patch, not a hardware installation of an immobilizer. Therefore, physical deterrents are often required to prevent the window-smash that occurs before the thief realizes the software is updated.

The Hierarchy of Intervention

The following guide outlines what owners should prioritize to stabilize their Hyundai Insurance Rates.

| Intervention Level | What to Look For (Effective) | What to Avoid (Ineffective) |

|---|---|---|

| Software | Official Dealer "Anti-Theft Logic" Update (Free). | Assuming the 2022 patch was automatic (Must visit dealer). |

| Physical Deterrent | Steering Wheel Lock (The Club) or Brake Lock. | Window stickers alone (Thieves ignore these). |

| Aftermarket Security | Compustar/Viper Alarm with Glass Break Sensors. | Cheap "flashing light" decoys. |

| Insurance Strategy | Shopping independent brokers for "bundling" discounts. | Auto-renewing without checking current market rates. |

Implementing these physical and digital barriers provides the documentation necessary to challenge premium hikes during your next renewal period.

Conclusion: Navigating the New Insurance Landscape

The spike in Hyundai Insurance Rates serves as a critical lesson in the automotive industry: security is not a luxury feature, but a fundamental determinant of asset value. For owners of affected models, the path forward requires a proactive combination of dealer-installed software updates and highly visible physical deterrents. While the "Kia Boyz" trend may eventually fade, the insurance data suggests that premiums for non-immobilizer vehicles will remain elevated for the foreseeable future. Action must be taken now to protect both the vehicle and the owner’s financial standing.

Read More